Quick answer:

Surrogacy in Florida typically costs between 110,000 and 200,000 dollars, but insurance compatibility can change total expenses by 15,000 to 40,000 dollars or more. The surrogate’s maternity insurance is one of the biggest financial swing factors in the entire journey.

Families who understand insurance early avoid the most expensive surprises.

This guide explains how insurance actually affects Florida surrogacy costs, what scenarios families should budget for, and how to verify coverage before matching with a surrogate.

Table of contents

- Quick answer: Surrogacy cost with insurance in Florida

- Why insurance is the biggest cost variable in Florida surrogacy

- How to verify a surrogate’s insurance before matching

- What insurance does not cover in surrogacy

- Hidden insurance related costs families often miss

- Florida specific insurance considerations

- Frequently asked questions about surrogacy insurance in Florida

- Final thoughts: Insurance determines the real budget

Quick answer: Surrogacy cost with insurance in Florida

| Scenario | Estimated total range |

|---|---|

| Surrogate has compatible maternity insurance | 110,000 to 150,000 |

| Insurance requires supplemental gap policy | 130,000 to 180,000 |

| No insurance coverage available | 150,000 to 200,000+ |

These totals include surrogate compensation, agency coordination, legal services, IVF medical expenses, and pregnancy related insurance exposure.

Most Florida families plan 15,000 to 25,000 dollars for pregnancy insurance. Higher totals usually appear only when a surrogate lacks compatible coverage or when extended hospitalization is required. Understanding this range helps families plan confidently without assuming worst case scenarios.

Families comparing insurance exposure should also review our total surrogacy cost guide to understand how insurance fits into the full journey budget.

Why insurance is the biggest cost variable in Florida surrogacy

Insurance is not a minor line item. It determines whether pregnancy costs are partially absorbed by an existing plan or funded privately.

Variation comes from

- policy exclusions for surrogacy

- self funded employer plans with custom rules

- maternity riders and coverage limits

- high deductibles and network restrictions

- policy language that treats surrogacy differently than traditional pregnancy

Two healthy surrogates can create very different budgets based solely on insurance structure. This is why professional insurance review happens before a match is finalized.

A deeper explanation of surrogacy insurance coverage helps families understand why policy compatibility matters so early in planning.

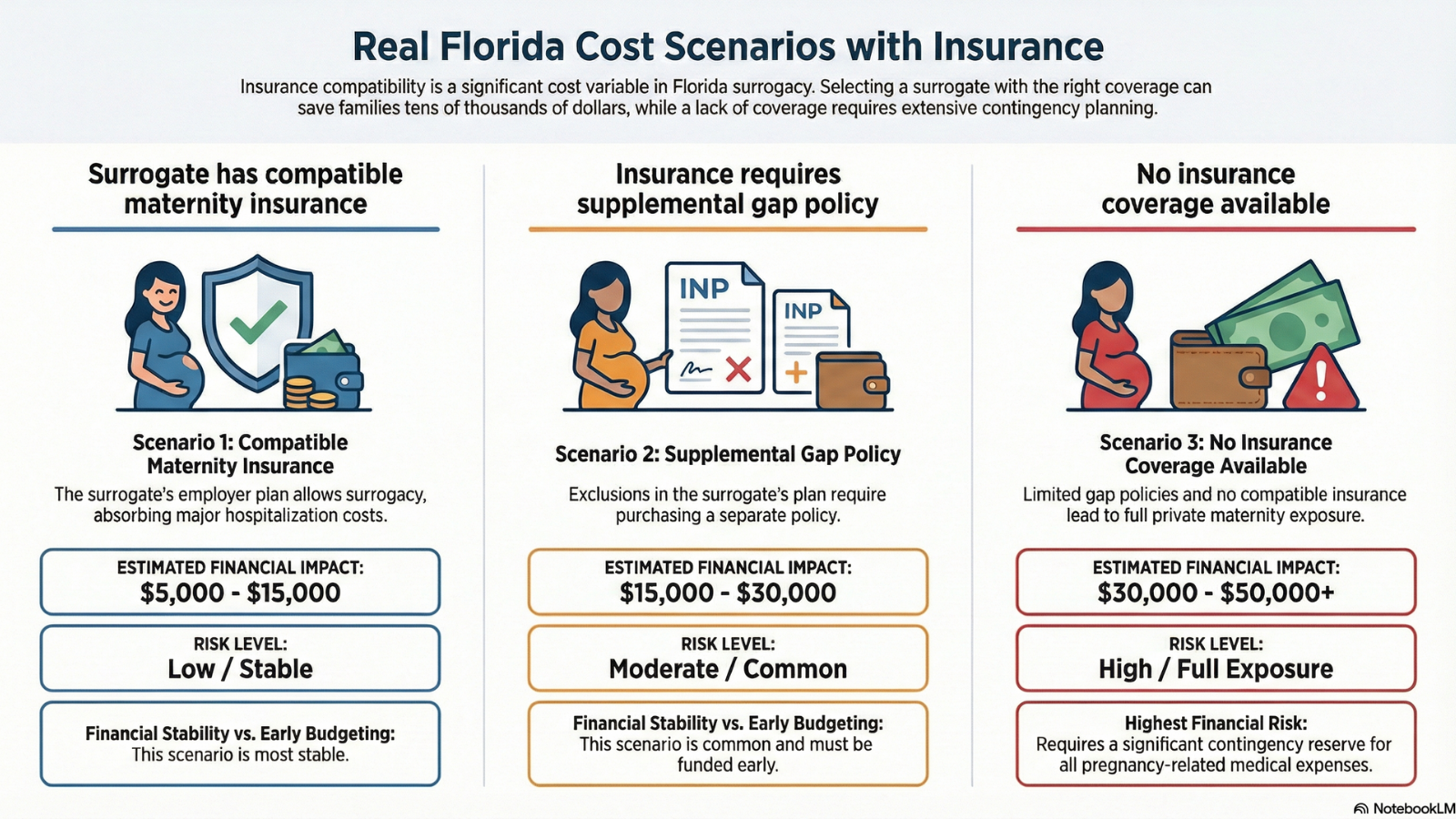

Real Florida cost scenarios with insurance

Scenario 1: Surrogate has compatible maternity insurance

The surrogate’s employer plan allows gestational surrogacy.

Families budget for deductibles and uncovered services, but major hospitalization costs are partially absorbed.

Estimated insurance impact

5,000 to 15,000 dollars

This is the most financially stable scenario and is prioritized during responsible surrogate screening.

Scenario 2: Insurance requires supplemental gap policy

The surrogate’s plan contains exclusions that require additional maternity protection.

A supplemental gap policy restores financial predictability.

Estimated insurance impact

15,000 to 30,000 dollars

This is the most common Florida scenario and is planned for early in the journey.

Scenario 3: No insurance coverage available

No compatible maternity insurance exists and gap policies are limited.

Families prepare for private maternity exposure.

Estimated insurance impact

30,000 to 50,000+ dollars

This scenario requires a larger contingency reserve but is fully manageable with transparent budgeting.

Insurance planning works together with surrogate compensation, which is explained in our Florida surrogate cost breakdown.

How to verify a surrogate’s insurance before matching

Insurance review should happen before emotional commitment.

Families should confirm:

- Does the policy explicitly allow gestational surrogacy

- Is the plan self funded or fully insured

- What are the maternity deductibles

- Are hospitals in network for delivery

- Are complications covered

- Can coverage change mid pregnancy

An experienced agency coordinates professional insurance review to prevent late stage financial shocks.

What insurance does not cover in surrogacy

Even excellent policies do not cover:

- travel expenses

- lost wages

- childcare during appointments

- bed rest support

- household assistance

- legal fees

- NICU lodging costs

- recovery stipends

These remain part of surrogate compensation packages and pregnancy reimbursements.

Insurance reduces exposure. It does not eliminate budgeting responsibility.

Hidden insurance related costs families often miss

Families frequently overlook:

- out of network hospital billing

- emergency transfer costs

- policy cancellation risk

- extended hospitalization

- multiple embryo transfers

- pregnancy complications

- deductible resets during calendar year changes

Responsible planning includes contingency reserves beyond base insurance estimates.

Florida specific insurance considerations

Florida is a surrogacy friendly state legally, but insurance behavior still varies by employer and carrier.

Common patterns include:

- self funded corporate plans with unique exclusions

- regional hospital network limitations

- policy language ambiguity requiring legal review

- maternity billing differences across clinics

Families working with Florida based agencies benefit from localized insurance experience and established review processes.

Families evaluating financial risk should understand how choosing a surrogacy agency affects insurance review and cost stability.

Frequently asked questions about surrogacy insurance in Florida

Does insurance cover surrogacy in Florida

Sometimes. Coverage depends on the surrogate’s employer plan and policy language.

How much does insurance reduce surrogacy cost

Compatible coverage can reduce expenses by 15,000 to 40,000 dollars or more.

What happens if the surrogate loses insurance mid pregnancy

Backup planning and escrow reserves protect against sudden exposure.

Can intended parents buy insurance for the surrogate

In some cases gap policies are available, but options depend on eligibility.

Is maternity insurance required for surrogacy

Professional agencies strongly recommend insurance review before embryo transfer.

Final thoughts: Insurance determines the real budget

Surrogacy cost discussions that ignore insurance are incomplete.

Insurance compatibility is not a technical detail. It is one of the primary drivers of financial risk and stability.

Families who verify coverage early make stronger decisions, avoid emergency budgeting, and protect the emotional integrity of the journey.

Understanding insurance is not optional. It is part of responsible planning.